Common Stock: Mako Mining (TSXV: MKO, OTC: MKAOF)

Current Market Price: $.34

Market Capitalization: $198 million

**Note: The company is in the process of changing its fiscal year. All references to “2019” in this document refer to the 8-month period from may 1 2019 to December 31 2019.

Mako Mining Stock – Summary of the Company

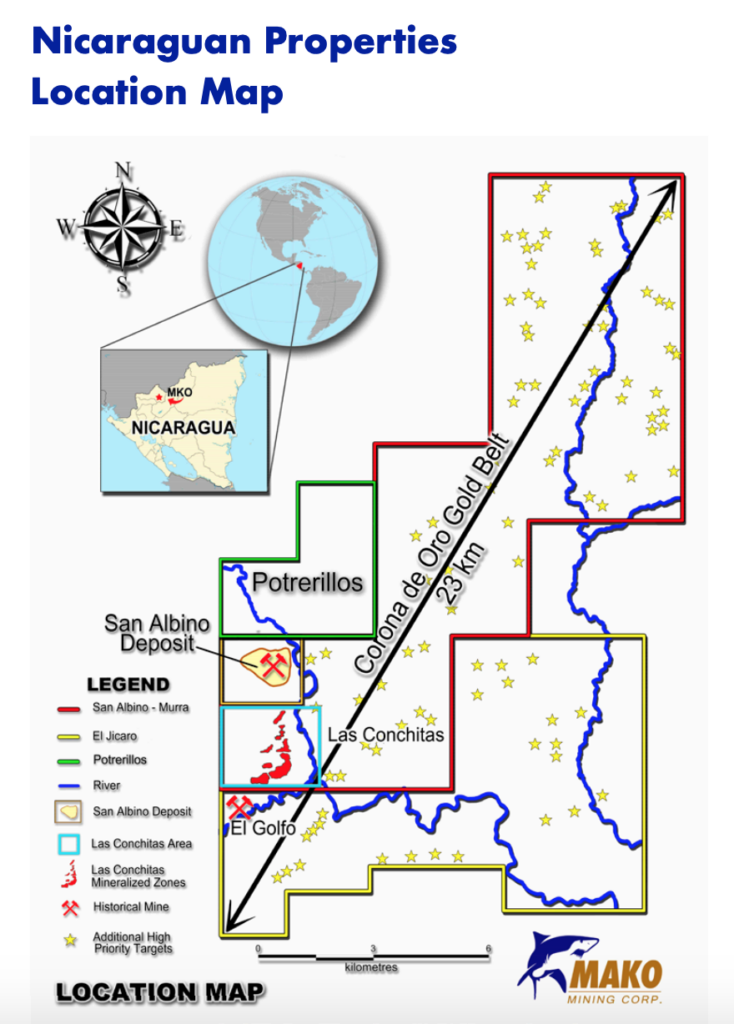

Mako Mining is a gold mining company focused on the acquisition, development, exploration, and operation of gold mining properties in Mexico and Nicaragua. They own one major exploration stage property in Nicragua, the San-Albino Property. Mako Mining was founded in 2004 and is headquartered in Vancouver Canada.

Revenue and Cost Analysis

In 2018 Mako purchased Marlin mining, prior to this acquisition Mako had no revenue. In 2019 Mako recognized revenue from the Marlin acquisition, but halted operations at their only producing mine in Mexico. Currently the company is solely focused of the San Albino property in Nicaragua, which does not currently have revenue.

In 2019, the company had a net loss of $8.5 million. The net loss was overstated due to a significant one time inventory write down of $8.6 million. This write down is from lost inventories due to the company ceasing is leach pad operations in Mexico.

Mako has significant exploration expenses which totaled $4.1 million in 2019.

Mako Mining Stock – Royalty and Streaming Agreements

The San Albino property has a 2% net smelter royalty that will be paid to Sailfish Royalty company. In addition, Sailfish has a streaming agreement that gives them the right to purchase 4% of the production at San Albino at 25% of the spot price.

There is also a net smelter royalty payable to the Nicaraguan government based on the current mining laws in the country.

Balance Sheet Analysis

Mako does not have a strong balance sheet, liquidity levels are low and the company stated that based on their current burn rate, they will need to raise additional funds in the short term.

At the end of 2019 current assets totaled $7.8 million, including $4.2 million in cash. Current liabilities were $11.8 million.

The company’s largest asset is a long-term mineral property valued at $10 million. Total assets were $18 million at the end of 2019. Total liabilities were $13.4 million, most of which is current accounts payable of $10.4 million.

Mako Mining – Debt Analysis

On February 20, 2020, the Company closed a $15.15 million unsecured term loan and intends to use these funds for construction, development and exploration activities in Nicaragua, for general corporate purposes, and for fees and expenses incurred in connection with the loan.

Mako Mining Stock – Share Dynamics and Capital Structure

As of April 2020, Mako had 583.7 million shares outstanding. They also have 50.1 million options outstanding. Fully diluted shares outstanding is 633.8 million shares.

Mako has a dilutive capital structure. The company will need to raise additional capital and if they do so via equity, existing shareholders will be further diluted. Investors should carefully consider their place in the capital structure and the effects of dilution before investing.

Mako Mining Stock – Dividends

The company does not pay a dividend an is unlikely to do so in the short term.

Management – Skin in the game

Over the past 12 months insiders have been net buyers of Mako stock. This is generally viewed as a bullish signal.

Mako Mining – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

$13.5 million/ $5.1 million = 2.6

A debt to equity ratio of 2.6 indicates that Mako is financed to a significant extent with debt. They may be reliant on additional debt financing in the future.

Price to Book Ratio

Current Share Price/Book Value per Share.

$.34/$.01=34

Based on my estimate of fully diluted shares outstanding Mako has a book value per share of $.01. At the current market price this implies a price to book ratio of 34. A price to book ratio of 34 means Mako stock trades at a very high premium to the book value of its assets.

Working Capital Ratio

Current Assets/Current Liabilities

$7.7 million/$11.8 million = .66

A working capital ratio of .66 indicates a weak short term liquidity position, meaning the company may have difficulties meeting its short-term obligations.

Gold Market – Economic Factors and Competitive Landscape

Gold mining is a highly competitive, capital intensive business. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear gold companies are poised to benefit from a strong economic tailwind.

Mako Mining Stock – Summary and Conclusions

The San Albino property is a very promising property in an under owned and risky jurisdiction. If Mako is able to establish a foothold in Nicaragua and develop both the San Albino property and other claims, then the upside for shareholders could be significant.

However, some of this upside has already been sold in the form of royalty and streaming arrangements. Mako is currently in a weak financial position. It lacks the necessary liquidity to fund it operations and repay a significant obligation related to the discontinued Mexico operation. Meaning they will need to raise more capital.

Mako already has a dilutive capital structure, and raising additional capital, weather debt or equity, will be to the detriment to existing shareholders.

Although the company has significant upside in the best-case scenario, the current valuation looks expensive given the jurisdictional, financial, and dilution risks for what is as of now a single asset company.

For these reasons, I will not be investing in Mako stock yet, but I will continue to monitor the company and reconsider based on new developments.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.