Common Stock: Excellon Resources (TSX:EXN)

Current Market Price: $.54 USD

Market Capitalization: $83.3 million USD

Excellon Resources Stock – Summary of the Company

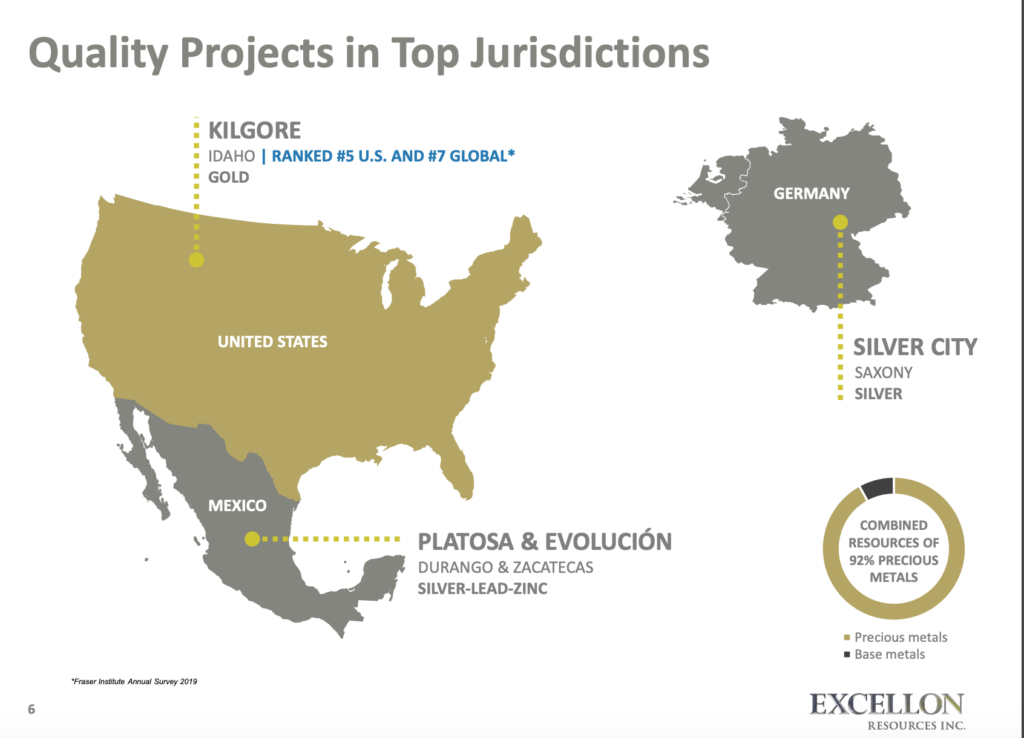

Excellon Resources is a silver mining company focused primarily on the exploration and operation of its 100% owned Platosa Mine in Mexico. They also own other exploration stage properties in Mexico, Germany, and The United States. Excellon was founded in 1987 and is headquartered in Toronto, Canada.

Revenue and Cost Analysis

In 2019 Excellon produced 1 million ounces of silver, 6.1 million pounds of lead, and 8.4 million pounds of zinc. Their average realize price per silver ounce sold was $16.07, compared to an all in sustainable cost per ounce sold of $23.57.

Total revenue in 2019 was $26.5 million, an increase from $24.3 million in 2018. The company had a net loss of $10.1 million in 2019, significantly higher than their $7.7 million net loss in 2018.

Excellon continues to spend relevant amounts on exploration. Exploration costs were $3.9 million in both 2019 and 2018.

Excellon Resources – Royalty and Streaming Agreements

The Mexican government is entitled to a 7.5% royalty based on EBITDA. However, from an accounting perspective the company treats this as an income tax, not a royalty expense.

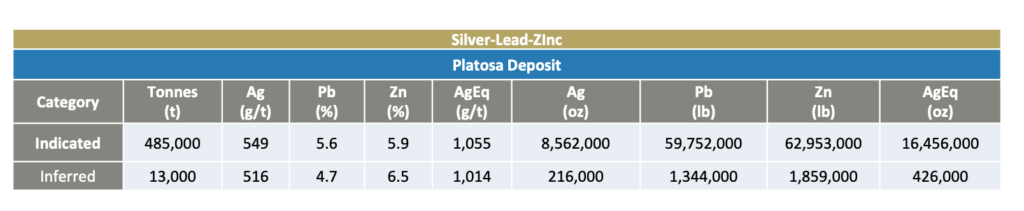

Excellon Resources – Mineral Resources

The Platosa property has “Indicated and Inferred” resources of 8.5 million and 216 thousand ounces of silver respectively.

Balance Sheet Analysis

Excellon has a descent balance sheet with sufficient liquidity and low long term liabilities.

Excellon Resources – Debt Analysis

As of year-end 2019, the company does not have any debt outstanding. The do have a small long term lease liability.

Excellon Resources Stock – Share Dynamics and Capital Structure

As of March 2020, the company had 113.2 million common shares outstanding. They also have options, warrants, and restricted share units outstanding. Fully diluted shares outstanding is 125.4 million shares.

Excellon Resources Stock – Dividends

The company does not currently pay a dividend.

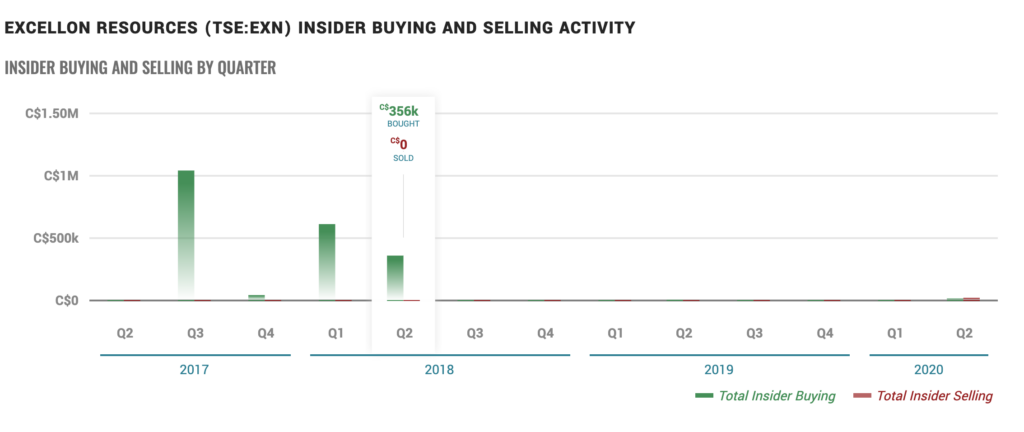

Management – Skin in the game

Insiders at Excellon purchased significant amounts of the company’s stock in 2017 and 2018, but have not made any relevant purchases recently. Insider buying is generally viewed as a bullish signal for a stock.

Excellon Resources Stock – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

$13 million/ $43 million = .3

A debt to equity ratio of .3 indicates the Excellon does have relevant debt in its capital structure, but relies mostly on equity financing to fund itself.

Price to Book Ratio

Current Share Price/Book Value per Share.

$.54/$.34 = 1.6

Based on fully diluted shares outstanding, Excellon has a book value per share of $.34. At the current market price this implies a price to book ratio of 1.6, meaning the company’s stock currently trades at a slight premium to the book value of the company.

Working Capital Ratio

Current Assets/Current Liabilities

$16.8 million/$9.1 million = 1.8

A working capital ratio of 1.8 indicates sufficient short term liquidity. Excellon should not have a problem meeting its obligations in the near term.

Silver Market – Economic Factors and Competitive Landscape

Silver mining is a highly competitive, capital intensive business. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear silver companies are poised to benefit from a strong economic tailwind.

Excellon Resources Stock – Summary and Conclusions

Excellon has a producing mine in Mexico and several promising exploration stage projects. The company has low long term liability levels and sufficient near term liquidity. Their capital structure is fairly dilutive.

Most concerning is the company’s operating loss. Even with the recent price increases in silver, their cost of production is still well above the silver price, meaning the will continue to run an operating loss.

The company has significant exploration potential, including at the already producing Platosa property, which is huge. However, I would like to see their operating results improve before making an investment. Management has stated cost reduction is goal, so I will wait to see if they deliver results. If they can bring production costs closer to break even, I will reconsider investing, as I like their exploration portfolio.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.