Common Stock: Omineca Mining and Metals (TSXV: OMM)

Current Market Price: $.35 CAD

Market Capitalization: $20.5 million CAD

**Note: All values in this article are expressed in Canadian Dollars (CAD) unless otherwise noted.

Omineca Mining Stock – Summary of the Company

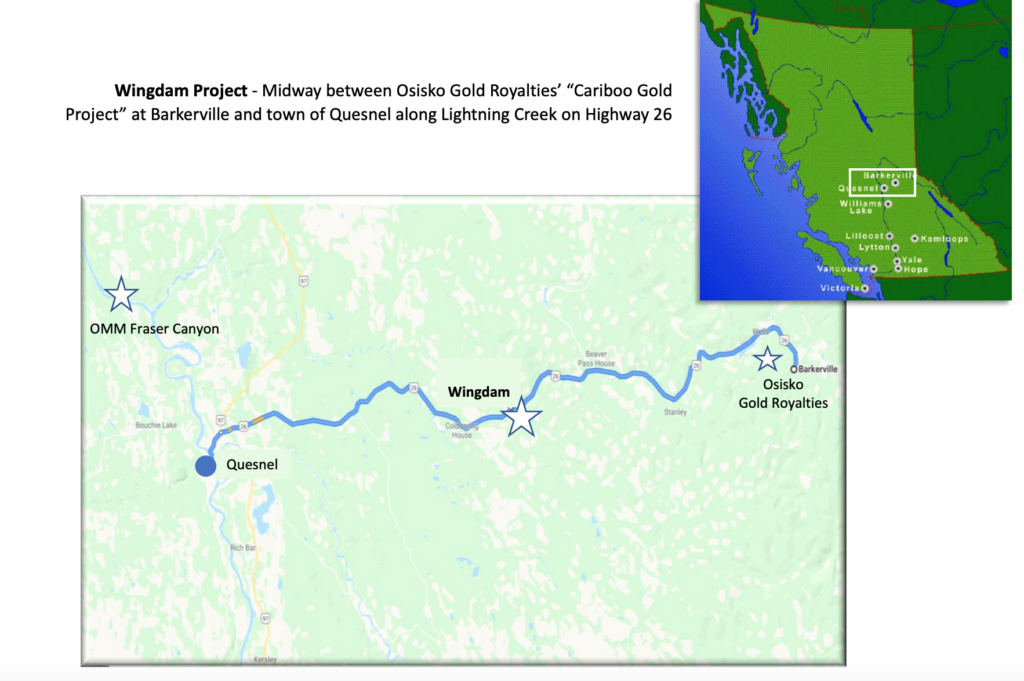

Omineca Mining and Metals is a mineral resource company focused on the acquisition and exploration of precious metals properties in Western Canada. Their keystone project is the Wingdam Gold project in British Columbia. They also own several other exploration stage properties. The company was founded in 2011 and is headquartered in Alberta, Canada.

Revenue and Cost Analysis

The company does not have any properties that are currently producing and therefore does not have any revenue. Omineca consistently runs a net loss and is likely to continue to do so for the foreseeable future.

In 2019, they had a net loss of $580 thousand. Their largest expenses were administrative, including wages.

Omineca Mining – Royalty and Streaming Agreements

The Wingdam project has a 1% net smelter royalty attached. Several of the company’s other properties also have net smelter royalty’s ranging from 2% to 2.5%.

Balance Sheet Analysis

Omineca has a weak balance sheet with very low liquidity and high liability levels, including excessive debt. They have a working capital ratio of .22, which indicates a very weak liquidity position. The company may have problems meeting its short-term liabilities. In addition, they have a negative book value, meaning their liabilities exceed their assets.

Omineca Mining – Debt Analysis

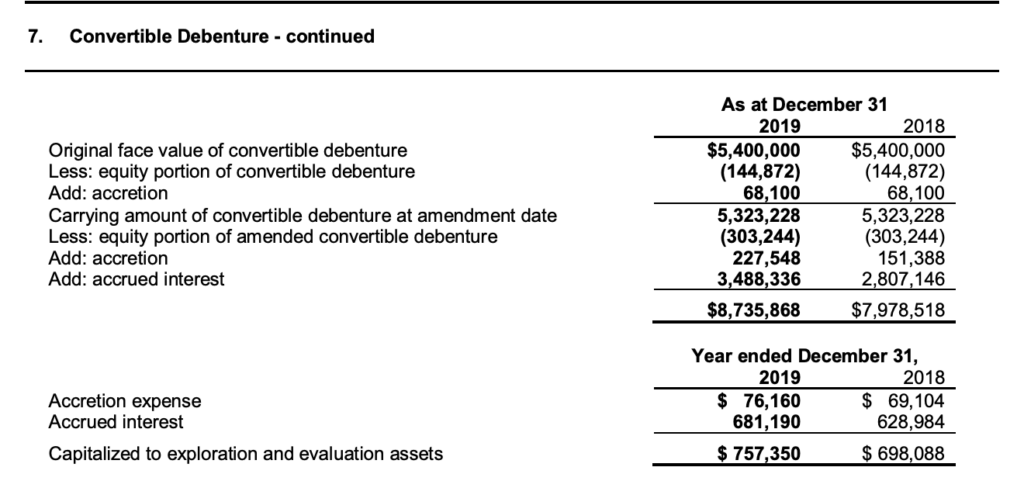

As of year-end 2019, the company had $8.7 million in convertible debt outstanding. In my opinion this is excessive given the company’s stage in their life cycle.

Omineca Mining Stock – Share Dynamics and Capital Structure

As of April 2020, the company had 90.1 million common shares outstanding. In addition, they have 8 million options and 16.2 million warrants outstanding. Fully diluted shares outstanding is around 114.2 million shares.

Omineca has an unfavorable capital structure for common stock holders. Investors should carefully consider their place in the capital structure before investing.

Omineca Mining Stock – Dividends

The company has never paid a dividend and is unlikely to do so for the foreseeable future.

Management – Skin in the game

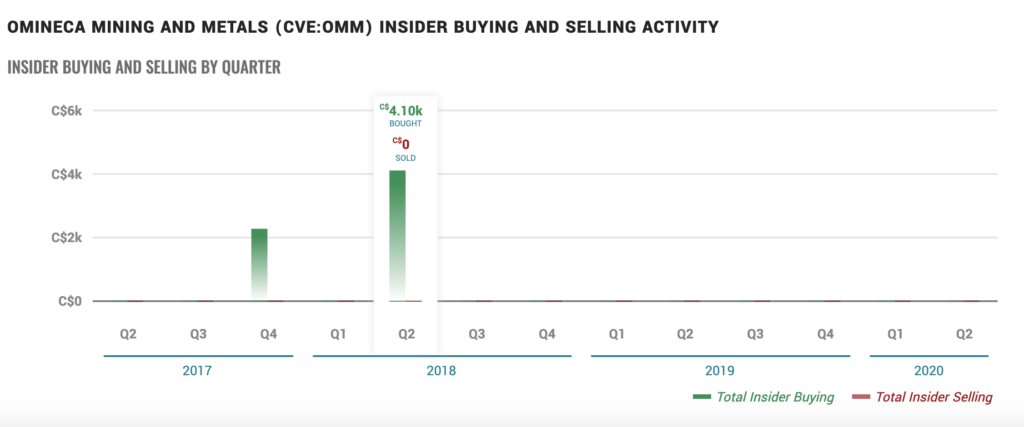

There has not been any relevant insider activity related to Omineca stock recently, providing no signal for investors.

Gold Market – Economic Factors and Competitive Landscape

Gold mining is a highly competitive, capital intensive business. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear gold companies are poised to benefit from a strong economic tailwind.

Omineca Mining Stock – Summary and Conclusions

The company’s main project has been in care and maintenance since 2012 and according to the company the quantity and quality of the deposits are “conceptual in nature”, as exploration has been insufficient. Management has had over 7 years to advance this project and has been unable to do so. I wouldn’t expect this to change anytime soon.

In addition, the company is in very poor financial health and has a dilutive capital structure, unfavorable to common stock investors.

For these reasons, I will not invest in Omineca Stock.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.