Common Stock: Mills Solaris (MILS3)

Current Market Price: R$ 6.15

Market Capitalization: R$ 1.5 billion

*All values in this article are expressed in Brazilian Reais (BRL) unless otherwise noted.

**The bulk of this analysis is based on the company’s most recent audited financial report, which can be found by following this link.

Mills Stock – Summary of the Company

Mills Solaris is a construction equipment rental company specialized on equipment for “at height” engineering projects. They operate throughout Brazil and employ around 1,200 people. Mills was founded in 1952 and is headquartered in Rio de Janeiro Brazil.

Revenue and Cost Analysis

Mills had revenue of R$ 439.5 million in 2019. Their COGS was R$ 282.5 million, representing a gross margin of 36%. The newly combined company was not profitable in 2019 and had a net loss of R$ 45 million.

Mills and Solaris Merger

In May 2019 Mills merged its operations with Solaris. As a result of the business combination, 76,056,038 new common shares were issued by the company in favor of Solaris’ shareholders, who then received 0.4927615448 Mills’ shares for each 1 common share of Solaris.

Balance Sheet Analysis

Mills has a decent balance sheet. They have sufficient liquidity and reasonable liability levels.

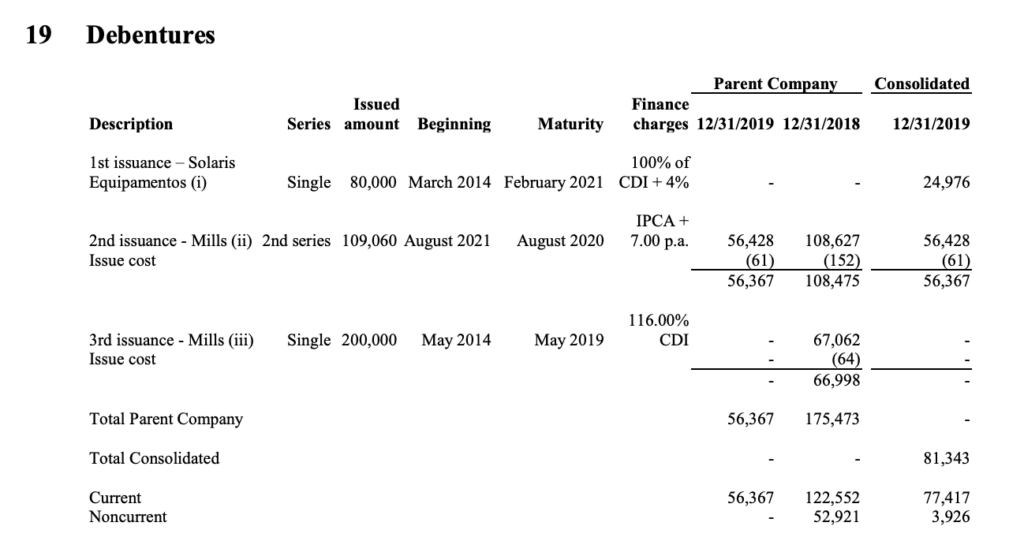

Mills – Debt Analysis

As of year-end 2019 Mills has total debt and financings outstanding of R$ 100 million, R$ 92.5 million of which is classified as current.

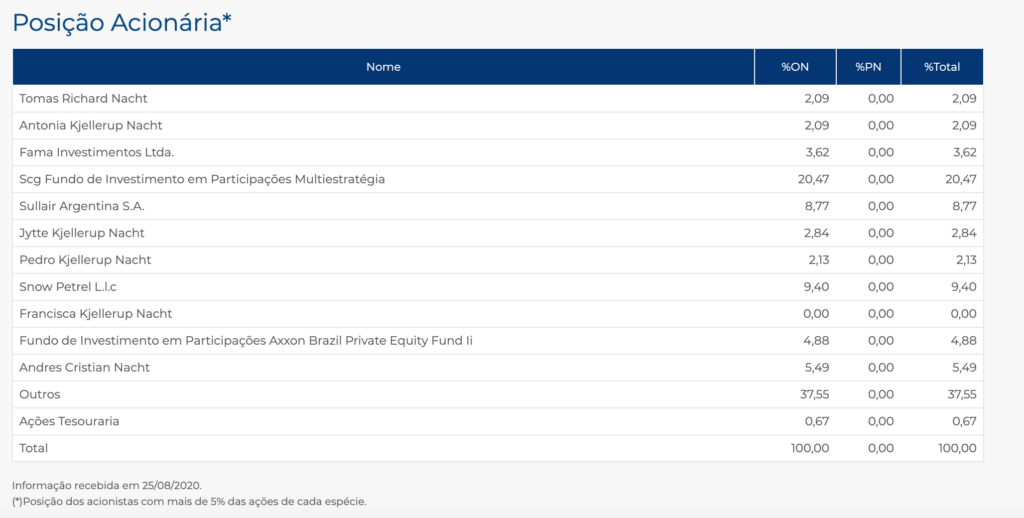

Mills Stock – Share Dynamics and Capital Structure

As of year-end 2019 Mills has 252 million common shares outstanding. Insiders and institutional investors own around 62% of the outstanding shares, with the remaining 38% being held by smaller investors with an ownership stake of less than 5%.

Mills Stock – Dividends

The company did not pay a dividend based on 2019’s results.

Mills Stock – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

R$ 268.5 million / R$ 1.1 billion = .24

A debt to equity ratio of .24 indicates that Mills uses a mix of debt and equity in its capital structure, but relies mostly on equity financing to fund itself.

Working Capital Ratio

Current Assets/Current Liabilities

R$ 306 million / R$ 174.2 million = 1.75

A working capital ratio of 1.75 indicates sufficient liquidity. Mills should not have a problem meeting its near term obligations.

Price to Book Ratio

Current Share Price/Book Value per Share.

R$ 6.15 / R$ 4.40 = 1.4

Mills has a book value per share of R$ 4.40. At the current market price this implies a price to book ratio of 1.4, meaning Mills stock currently trades at a slight premium to the book value of the company.

Mills Stock – Summary and Conclusions

The merger with Solaris in 2019 allowed Mills to gain scale and market share, increasing its presence throughout Brazil. However the combined company is still in poor financial health. They are not profitable and given the 2020 economic crisis, their financial position likely deteriorated further. Construction equipment is not a business I am particularly interested in and therefore I am not going to invest in Mills stock. There are other Brazilian equities on my watchlist that I find much more compelling, such as Klabin.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.