Common Stock: International Meal Company (MEAL3)

Current Market Price: R$ 3.43

Market Capitalization: R$ 982 million

*All values in this article are expressed in Brazilian Reais (BRL) unless otherwise noted.

**The bulk of this analysis is based on the company’s most recent audited financial report, which can be found by following this link.

International Meal Company Stock – Summary of the Company

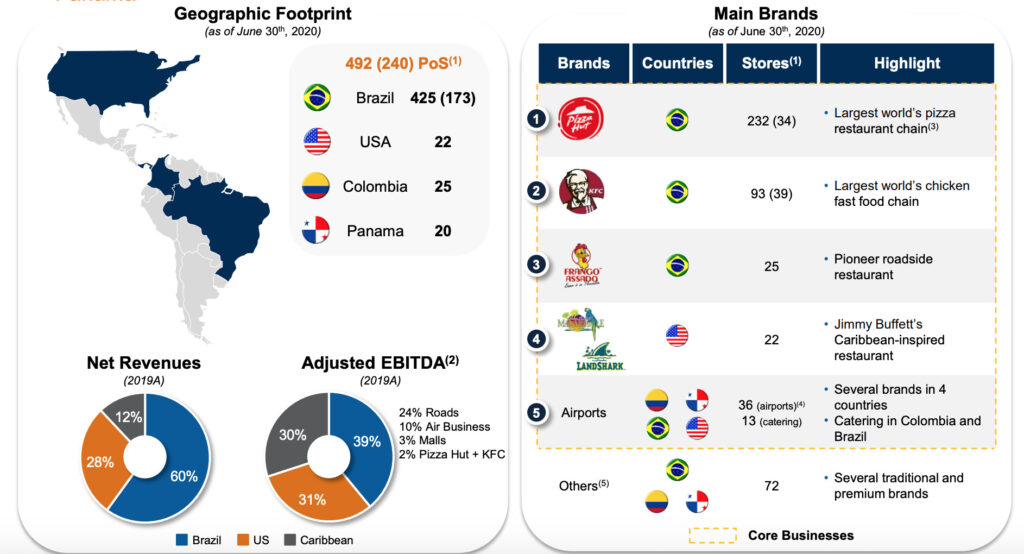

International Meal Company is a food and beverage company that sells their products to restaurants, snack bars, and coffee shops, focused on three principal areas; shopping malls, airports, and highways. In addition, they offer products for airline catering. They also operate restaurant franchises, the most well-known of which are Pizza Hut, Olive Garden, and Kentucky Fried Chicken (KFC).

The company operates in Brazil, Colombia, Panama, and The United States. International Meal Company was founded in 1965 and is headquartered in Sao Paulo, Brazil.

Revenue and Cost Analysis

International Meal Company had total revenue of R$1.6 billion in 2019, slightly higher than R$1.58 billion in 2018. The company had roughly equal COGS in 2019 and 2018, with a gross margin of 32% in both years.

The company was profitable in 2018 with net income of R$ 7.9 million, but had a loss of R$ 15.8 million in 2019. They were able to reduce selling expenses significantly in 2019, however large increases depreciation and financing expenses were mostly responsible for the company’s net loss in 2019.

The group does not have any one customer that accounts for more than 10% of revenue.

International Meal Company – Acquisitions

In 2019, International Meal Company Acquired MultiQSR. On the acquisition date (October 31, 2019), MultiQSR, through its subsidiaries, held: (a) 13 Pizza Hut restaurants in Brazil and the exclusive right to operate and sub franchise Pizza Hut restaurants in Brazil; and (b) 20 KFC restaurants in Brazil and the exclusive right to operate and sub franchise KFC restaurants in Brazil. In Brazil, MultiQSR owned and sub-franchised restaurants totaled 180 Pizza Hut restaurants and 46 KFC restaurants. The exclusive contract also allows MultiQSR to open a certain number of new restaurants.

Balance Sheet Analysis

International Meal Company has a decent balance sheet. They have a solid base of long term assets, mainly property, plant, and equipment. They also have a sufficient, but not strong, liquidity position. However, they also have significant debt and lease liabilities.

International Meal Company – Debt Analysis

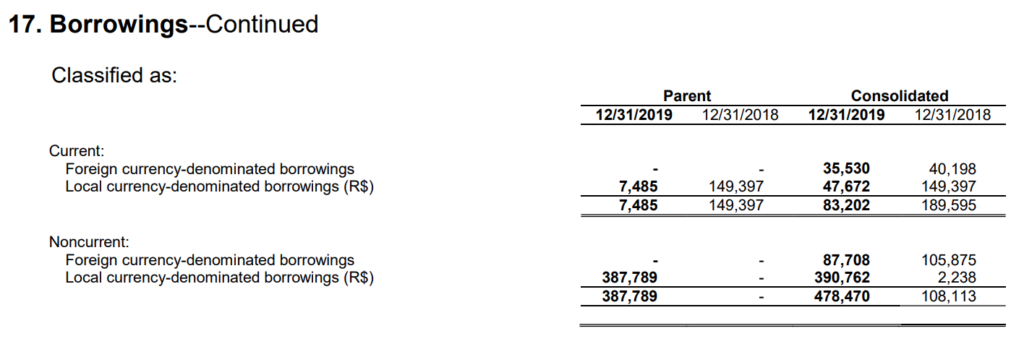

International Meal Company has a significant amount of debt outstanding. As of year-end the company had R$ 561.6 million in total debt outstanding, R$ 83.2 million of which is classified as current. They significantly increased their long-term debt in 2019.

It is also worth noting that a relevant portion of the company’s debt is denominated in foreign currency. However, they have operating revenues in four different currencies, providing a natural hedge to the carry trade.

International Meal Company Stock – Share Dynamics and Capital Structure

As of July 2020, the company has 286.4 million common shares outstanding. In addition, they have 9.3 million options outstanding. Fully diluted shares outstanding is around 295.7 million shares.

International Meal Company Stock – Dividends

The company paid a dividend in 2018, but did not pay a dividend in 2019.

Management – Skin in the game

I could not find any relevant insider activity in International Meal Company stock in the recent past, providing no signal for investors.

International Meal Company Stock – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

R$ 1.5 billion / R$ 1.1 billion = 1.3

A debt to equity ratio of 1.3 indicates that International Meal Company uses a mix of debt and equity in its capital structure, relying more heavily on debt to finance itself.

Working Capital Ratio

Current Assets/Current Liabilities

R$ 556.3 million / R$ 495 million = 1.1

A working capital ratio of 1.1 indicates a sufficient but not strong liquidity position.

Price to Book Ratio

Current Share Price/Book Value per Share.

R$ 3.43/ R$ 5.55 = .62

Based on fully diluted shares outstanding International Meal Company has a book value per share of R$ 5.55. At the current market price this implies a price to book ratio of .62, meaning the company’s stock trades at a significant discount to the book value of the company.

International Meal Company Stock – Summary and Conclusions

International Meal Company is a descent company. The have carved out a niche serving airports, malls, and rest stops in four countries. They operate under a wide range of franchisee brands and have been doing so successfully for decades. Their business is intriguing from a long term (10+ year) perspective, which matches up with my preferred time horizon.

However now is certainly not the time to invest in International Meal Company stock. The company has, and likely still is, getting crushed by the corona virus shut downs. Although the stock currently trades well below book value, it is doing so for a reason. The company has a significant debt burden and a portion of its assets are likely to be impaired. There is simply too much uncertainty related to the shut downs and the company’s financial position moving forward for me to invest.

I will wait to see their 2020 results and compare them to other Brazilian food companies such as Josapar, before I ever consider investing.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.