Common Stock: Amarillo Gold (AGC)

Current Market Price: $.215 CAD

Market Capitalization: $41 million CAD

**Note: All values in this article are expressed in Canadian Dollars (CAD) unless otherwise noted.

Amarillo Gold – Summary of the Company

Amarillo Gold Corporation is an exploration and development stage gold mining company. The company’s most advanced project is the Mara Rosa project. The Mara Rosa property is an open pit mine located in Goias Brazil. Amarillo also has an exploration stage property in Rio Grande do Sul, Brazil. Amarillo Gold is headquartered in Toronto, Canada.

Revenue and Cost Analysis

Amarillo Gold only has exploration stage projects; therefore, they do not have any revenue. In 2019, the company had a net loss of $4 million, a slight increase from a net loss of $3.87 million in 2018.

The company’s largest expenses are related to compensation and consulting services, followed by marketing and promotion expenses.

Amarillo Gold – Royalty and Streaming Agreements

The Mara Rosa Project will pay a 1% net smelter royalty to Franco Nevada and a 2.75% royalty to Royal Gold.

The project in Rio Grande do Sul has a total net smelter royalty of 3.5%.

Amarillo Gold – Reserves

The Mara Rosa project has 513,000 ounces of proven gold reserves and 574,000 ounces of probable gold reserves.

Balance Sheet Analysis

Amarillo Gold has a simple balance sheet consisting of mostly cash and a long-term resource asset. At the end of 2019 they had $7 million in cash and total assets of $40 million. Liquidity is sufficient in the short term. Current liabilities totaled $1.6 million, most of which is accounts payable.

Debt Analysis

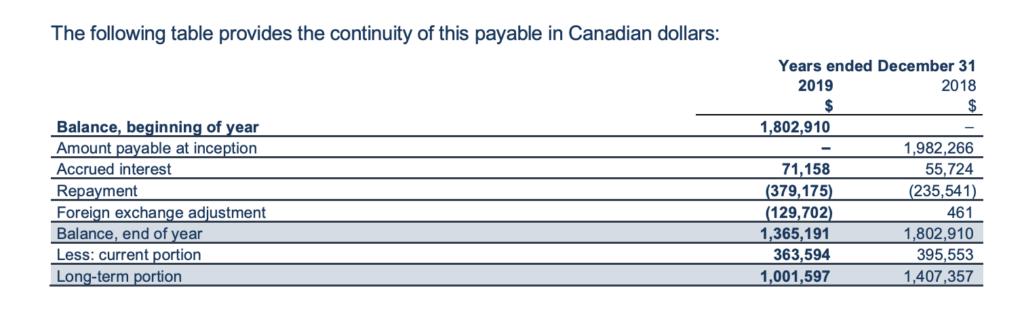

As of year-end 2019 Amarillo had repaid all its outstanding debt, but does have a concession fee outstanding related to litigation. This liability is carried at a value of $1 million.

Amarillo Gold Stock – Share Dynamics and Capital Structure

Amarillo Gold has a highly dilutive capital structure. As of March 2020, the company had 191.4 million common shares outstands. Additionally, they have 99 million warrants outstanding, a large portion of which are exercisable at $.30, as well as 1.3 million options outstanding.

Fully diluted shares outstanding totals 299.8 million shares.

Amarillo Gold Stock – Dividends

Amarillo Gold does not currently pay a dividend an is unlikely to do so in the short to medium term.

Management – Skin in the game

Over the last 12-18 months’ insiders at Amarillo gold have been net purchasers of the stock and insiders own a significant portion of the outstanding shares, around 19%. Additionally, in the past, the executive chairman has been willing to personally lend to the company.

This is generally considered a good signal for the stock as it implies interests between shareholders and management are aligned.

Amarillo Gold – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

$2.6 million/$37.6 million=.06

A debt to equity ratio of .06 means the company is funded almost entirely with equity capital.

Price to Book Ratio

Current Share Price/Book Value per Share.

$.215/$.13 = 1.6

Based on my estimate of fully diluted shares outstanding, Amarillo Gold has a book value per share of $.13. At the current market price this implies a price to book ratio of 1.6. A price to book ratio of 1.6 means the company’s common stock trades at a premium to the book value of its assets.

Working Capital Ratio

Current Assets/Current Liabilities

$7.6 million/$1,6 million= 4.8

A working capital ratio of 4.8 indicates sufficient short term liquidity, meaning the company is likely to meet all its obligations in the near term.

Gold Market – Economic Factors and Competitive Landscape

Gold mining is a highly competitive, capital intensive business. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear gold companies are poised to benefit from a strong economic tailwind.

Amarillo Gold – Summary and Conclusions

Amarillo Gold has two promising properties in Brazil. Both projects are still in early stages and additional licensing hurdles exist. Given the business environment in Brazil, this licensing is likely to take longer than expected. The company has an adequate liquidity position and is likely to be able to fund itself in the short term.

However, the company is likely to require additional capital to continue exploration in the medium term and will certainty require additional capital to develop any projects to an operational stage. Their capital structure is already highly dilutive and additional capital raising will be detrimental to existing shareholders.

Although valuation levels appear attractive at current levels, significant warrants outstanding and significant royalty agreements severely limit the upside for existing shareholders. The project certainty has potential, but I would prefer to wait to see how the additional funds are raised or at least wait for some of the warrants to expire before investing.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.