Common Stock: Fortuna Silver Mines (NYSE:FSM)

Current Market Price: $4.63 USD

Market Capitalization: $851 million USD

Fortuna Silver Mines Stock – Summary of the Company

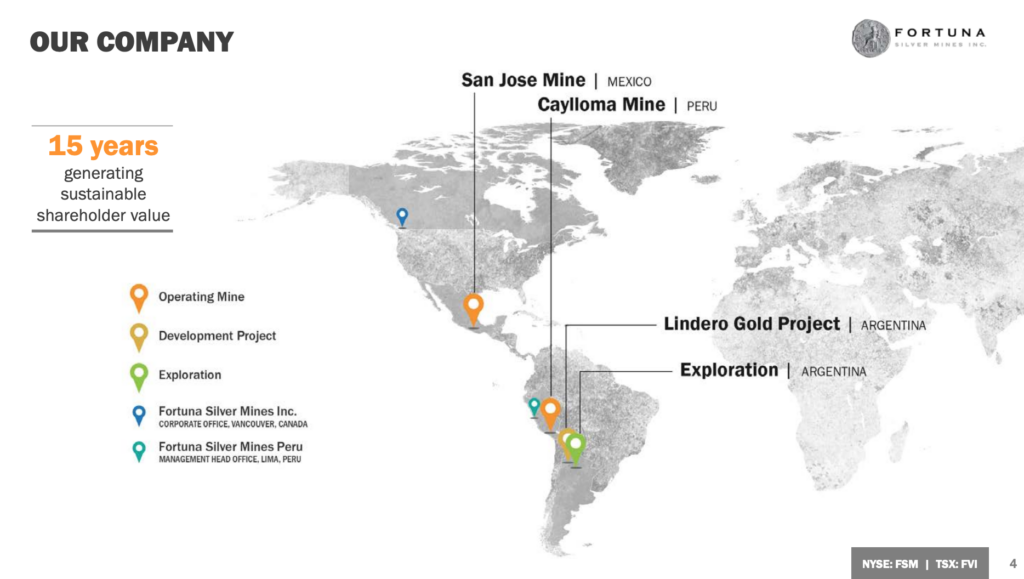

Fortuna Silver Mines is a mineral resource company engaged in the acquisition, exploration, and development of precious and base metal properties in Latin America. Its major properties are located in Mexico, Peru, and Argentina. Fortuna was founded in 1990 and is headquartered in Vancouver, Canada.

Revenue and Cost Analysis

Foutuna produced 8.8 million ounces of silver and 50,525 ounces of gold in 2019. They also produced relevant amounts of lead and zinc.

The company had total revenue of $257.2 million in 2019, a slight decrease from sales of $263.3 million in 2018. In 2019, operating income was $34.2 million and net income was $23.8 million.

Fortuna Silver Mines – Royalty and Streaming Agreements

The San Jose Mine has a 3% royalty payable on the sale of all minerals. This royalty is currently being disputed legally.

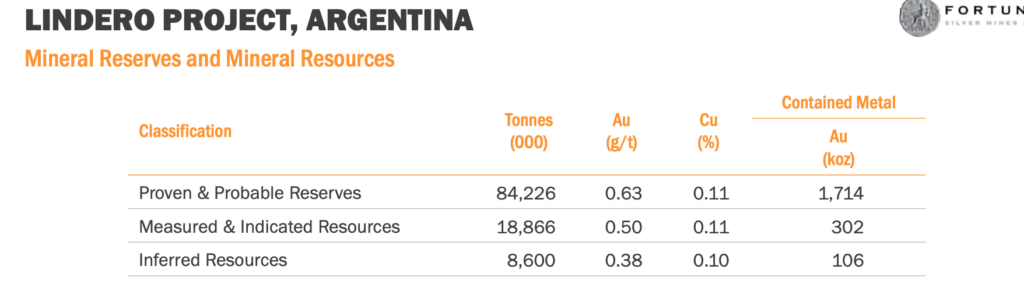

Fortuna Silver Mines – Mineral Resources

The Lindero project has “proven and probable” reserves of 1.7 million ounces of gold. The San Jose Mine in Mexico has “proven and probable” reserves of 203 thousand ounces of gold and 30.8 million ounces of silver. The Caylloma Mine in Peru has “proven and probable” reserves of 16 thousand ounces of gold and 6.4 million ounces of silver.

Balance Sheet Analysis

Fortuna has a solid balance sheet with sufficient liquidity and reasonable liability levels, considering the expenses incurred to construct the Lindero Mine.

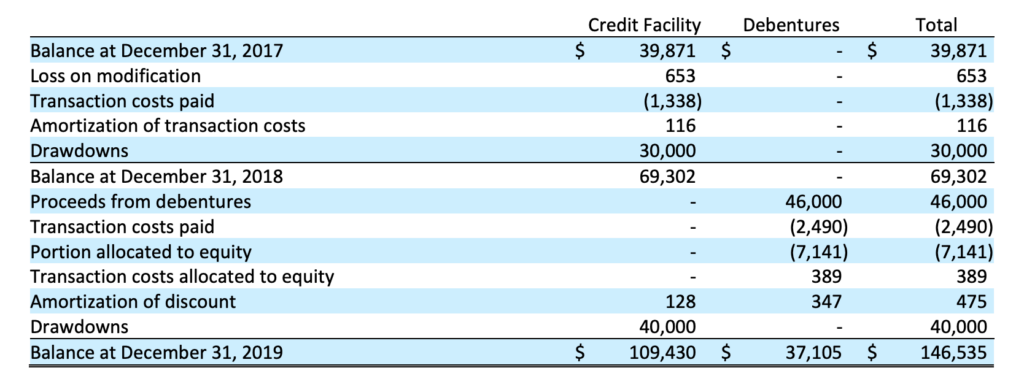

Fortuna Silver Mines – Debt Analysis

As of year-end 2019, total debt outstanding was $146.5 million. A significant increase from the previous year.

In October 2019, the company made a $46 million debt offering. The Debentures mature on October 31, 2024 and bear interest at a rate of 4.65% per annum, payable semi-annually in arrears on the last business day of April and October, commencing on April 30, 2020. The Debentures are convertible at the holder’s option into common shares in the capital of the Company at a conversion price of $5.00 per share, representing a conversion rate of 200 Common Shares per $1,000 principal amount of Debentures, subject to adjustment in certain circumstances.

Fortuna Silver Mines Stock – Share Dynamics and Capital Structure

As of May 2020, the company had 183.8 million common shares outstanding. In addition, they have restricted share units, options, and convertible debt outstanding. Fully diluted shares outstanding is 187.6 million shares.

Given the terms of the convertible debt offering discussed above, Fortuna has a dilutive capital structure with significant senior debt. Investors should carefully consider their place in the capital structure before investing.

Fortuna Silver Mines Stock – Dividends

The company does not currently pay a dividend.

Management – Skin in the game

Insiders at Fortuna Silver have been net buyers of the stock in recent past. This is generally viewed as a bullish signal.

Fortuna Silver Mines Stock – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

$300 million/$635.4 million = .47

A debt to equity ratio of .47 means that Fortuna uses a mix of debt and equity in its capital structure, but relies primarily on equity financing to fund itself.

Price to Book Ratio

Current Share Price/Book Value per Share.

$4.63/$3.39 = 1.4

Based on fully diluted shares outstanding, Fortuna has a book value per share of $3.39. At the current market price this implies a price to book ratio of 1.4, meaning Fortuna stock trades at a slight premium to the book value of the company.

Working Capital Ratio

Current Assets/Current Liabilities

$152.1 million/ $89.7 million = 1.7

A working capital ratio of 1.7 indicates sufficient liquidity. Fortuna should not have a problem meeting its near-term obligations.

Gold and Silver Markets – Economic Factors and Competitive Landscape

Gold and silver mining are highly competitive, capital intensive businesses. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear gold and silver companies are poised to benefit from a strong economic tailwind.

Fortuna Silver Mines Stock – Summary and Conclusions

Fortuna Silver is an intriguing company. They have a diversified portfolio of producing properties, with an additional gold property set to come into production in the near future. Management has proven effective in bringing mines into production. The company is financially healthy and looks to be able to operate sustainably for the foreseeable future. Additionally, the revenue mix between gold and silver is interesting.

My largest concerns are related to the capital structure, specifically dilution and debt. However, given the significant upside of the Lindero property, and the leverage the company has to rising gold and silver prices, I believe these risks to be acceptable.

I believe an allocation to FRM stock is acceptable for highly risk tolerant investors within a well-diversified gold stock portfolio.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.

3 Comments

Comments are closed.