Common Stock: Ascot Resources (TSX: AOT)

Current Market Price: $.80 CAD

Market Capitalization: $197.1 million CAD

**Note: All values in this article are expressed in Canadian Dollars (CAD) unless otherwise noted.

Ascot Resources Stock – Summary of the Company

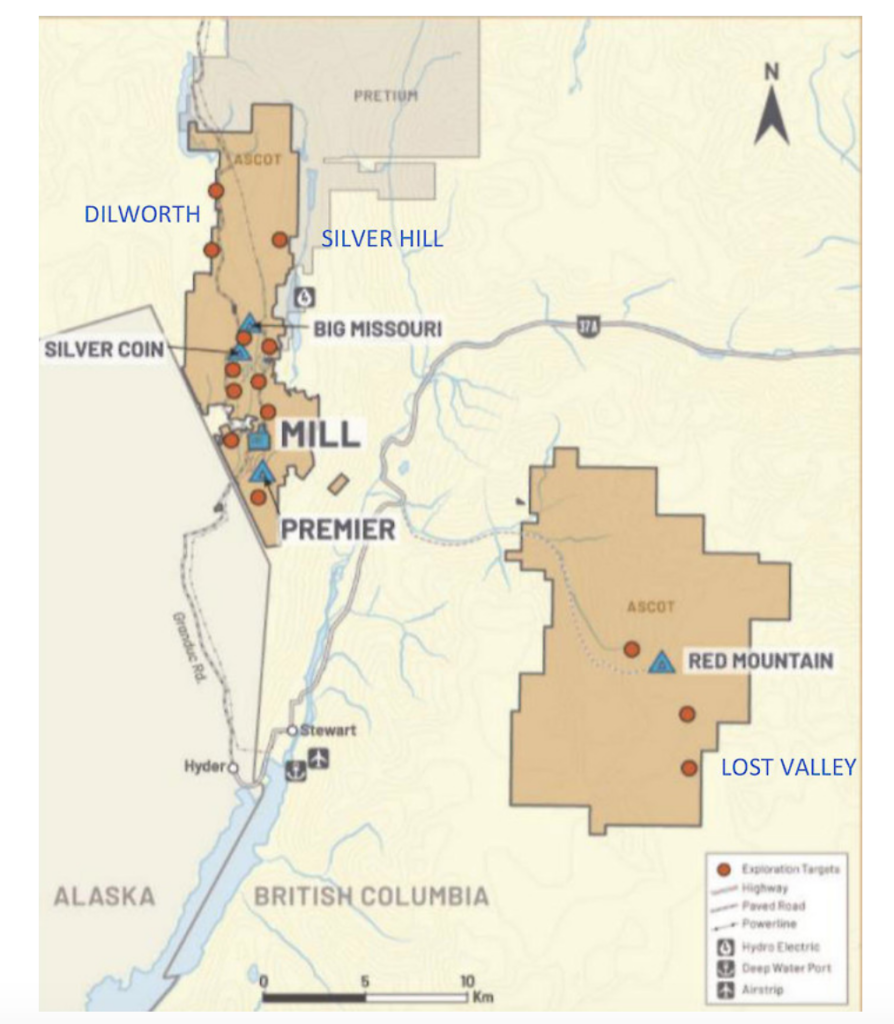

Ascot Resources is a mineral development and exploration company focused on restarting the previously producing Premier Gold Project in British Columbia. The project is currently in the exploration and development stage. They also have several other exploration stage properties in Canada. The company was founded in 1986 and is headquartered in Vancouver, Canada.

Revenue and Cost Analysis

Ascot does not have any properties that are currently producing and therefore does not have any revenue. The company consistently runs a net loss and will likely continue to do so for the foreseeable future.

In 2019, the company had a net loss of $7.8 million. Their largest expenses were compensation related, including share based compensation.

Ascot Resources – Royalty and Streaming Agreements

The Premier Project has net smelter royalties attached to certain claims on the property, ranging from 1% to 5%. Some of these royalties were inherited from the previous owner. The Red Mountain project has two separate net smelter royalty’s totaling 3.5%. The company’s Mt. Margaret project is subject to a 1.5% net smelter royalty.

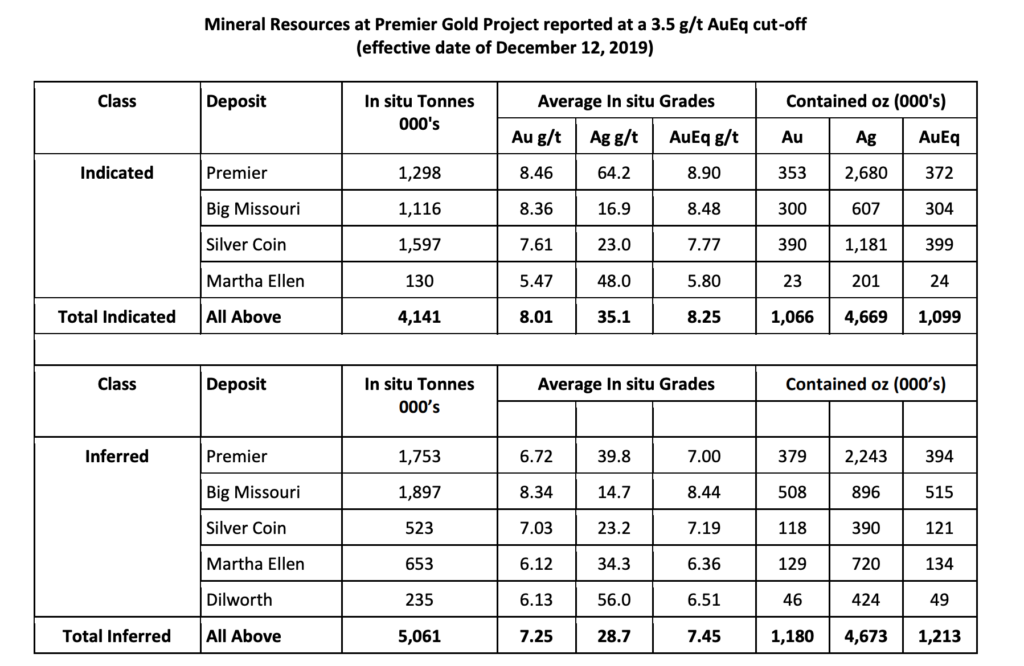

Ascot Resources – Mineral Resources

The company’s “Premier Gold Project” has estimated mineral resources of 1,066,000 ounces of gold and 4,669,000 ounces of silver in the Indicated category, and 1,180,000 ounces of gold and 4,673,000 ounces of silver in the Inferred category.

Their Red Mountain Project has an additional 544,000 and 1,747,000 measured ounces of gold and silver respectively, as well as 239,000 and 409,000 ounces of inferred gold and silver respectively.

Balance Sheet Analysis

Ascot has an OK balance sheet with good liquidity and what appears to be manageable liability levels. Short term liquidity is sufficient, but given the company’s burn rate they will likely need to raise additional capital in the future.

They have one major long term asset, an exploration and evaluation asset, valued at $169 million.

Ascot Resources – Debt Analysis

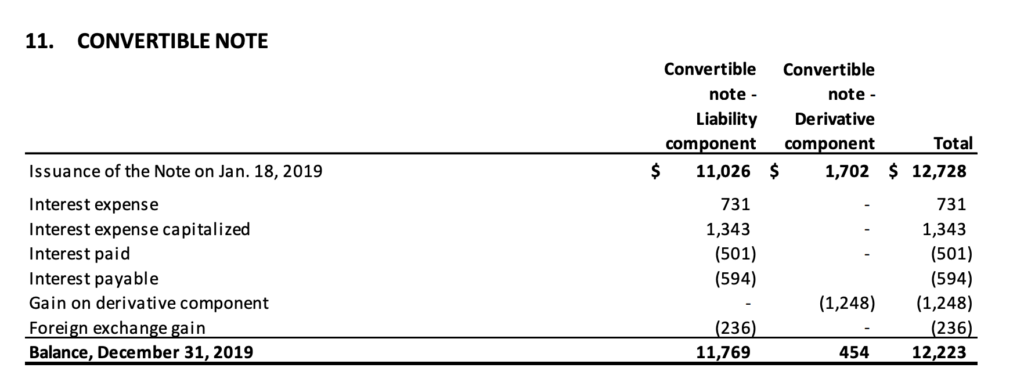

As of March 2020, the company had a convertible note outstanding valued at USD $10 million, which carries an interest rate between 8% and 8.5%. The conversion price is USD $1.13 per share.

Ascot Resources Stock – Share Dynamics and Capital Structure

As of March 2020, Ascot had 246.4 million common shares outstanding. In addition, they have 18.5 million options and 19 million warrants outstanding, as well as deferred and restricted share units. Fully diluted shares outstanding is around 284.5 million shares.

Ascot has a highly dilutive capital structure with convertible debt as well as other dilutive instruments outstanding. Investors should carefully consider their place in the capital structure before investing.

Ascot Resources Stock – Dividends

The company does not pay a dividend and is unlikely to do so for the foreseeable future.

Management – Skin in the game

Over the past 12-18 months’ insiders have been net buyers of Ascot Resources stock. This is generally viewed as a bullish signal for the stock.

Ascot Resources Stock – 3 Metrics to Consider

Debt to Equity Ratio

Total Liabilities/Total Share Holder Equity

$35.1 million/ $148.1 million = .23

A debt to equity ratio of .23 indicates that the company uses some debt in its capital structure, but mostly equity to finance itself. Ascot should not be overly reliant on any one form of financing moving forward.

Price to Book Ratio

Current Share Price/Book Value per Share.

$.80/$.53 = 1.5

Based on fully diluted shares outstanding Ascot has a book value per share of $.53. At the current market price this implies a price to book ratio of 1.5, meaning Ascot currently trades at a slight premium to the book value of the company.

Working Capital Ratio

Current Assets/Current Liabilities

$6.1 million/$3.1 million = 2

A working capital ratio of 2 indicates sufficient liquidity in the short term to meet obligations.

Gold Market – Economic Factors and Competitive Landscape

Gold mining is a highly competitive, capital intensive business. The company will need to compete fiercely for both new projects and capital. However, given the current economic environment of global money printing and zero or negative interest rates, it would appear gold companies are poised to benefit from a strong economic tailwind.

Ascot Resources Stock – Summary and Conclusions

Ascot has several promising properties in a proven mining region. Some of their properties have produced significant amounts of gold and silver in the past. The Premier Mine was at one point the largest gold mine in North America. Some infrastructure is already in place and the company’s goal is to restart the existing mines.

Although the properties are promising, I have doubts as to whether management will be able to bring any of them into production. The company ran a significant loss in 2019, and almost all its expenses were administrative and compensation related. In addition, the capital structure is highly dilutive and unfriendly to common shareholders. The company has senior convertible debt in addition to large amount of warrants and option outstanding. The amount of royalties sold on the properties is also concerning.

I have no doubt that Ascot has a high potential property. But given the unfavorable capital structure and managements lack of execution thus far, I am not willing to invest in Ascot stock at this time. However, I will continue to monitor the company and would reconsider investing if I can be more certain the mine will eventually be brought into production.

Disclaimer

This is not investment advice. Nothing in this analysis should be construed as a recommendation to buy, sell, or otherwise take action related to the security discussed. If I own a position in the security discussed, I will clearly state it.

This is not intended to be a comprehensive analysis and you should not make an investment decision based solely on the information in this analysis. I hope this serves as a useful starting point for a more comprehensive analysis, and hopefully draws attention to aspects of the company that were overlooked or merit further investigation. This is by no means intended to be a complete analysis. Again, this is not investment advice, do your own research.

One Comment

Comments are closed.